As the healthcare market moves toward a value-based care model, outpatient settings and services will only rise in demand from investors and patients alike. Ambulatory surgery centers, or ASCs, will be one of the most valuable assets in this shift in the healthcare industry. With several tailwinds driving the ASC investment market, including demographic and reimbursement benefits, a fragmented industry and the versatility of ASC services and specialties, investors should pay close attention to this market.

Market Overview & Players

According to the Ambulatory Surgery Center Association (ASCA), ASCs are healthcare facilities focused on providing same-day surgical care, including diagnostic and preventive procedures. They are specially designed as a more cost-effective and convenient alternative to hospital-based procedures, which could include overnight stays.

Based on data compiled by ASC Data, there are around 6,200 Medicare-certified ASCs in the United States, but more than 5,100 non-Medicare-certified ASCs (or 45%). Approximately half of the Medicare-certified facilities focus on a single specialty, such as orthopedic or pain, while many facilities are multi-specialty.

Orthopedics remains the most popular specialty, but gastroenterology, pain management and ophthalmology comprise significant portions of the ASC market. Cardiology has become the fastest-growing specialty as new technologies emerge and higher-acuity procedures continue to move to the ASC setting.

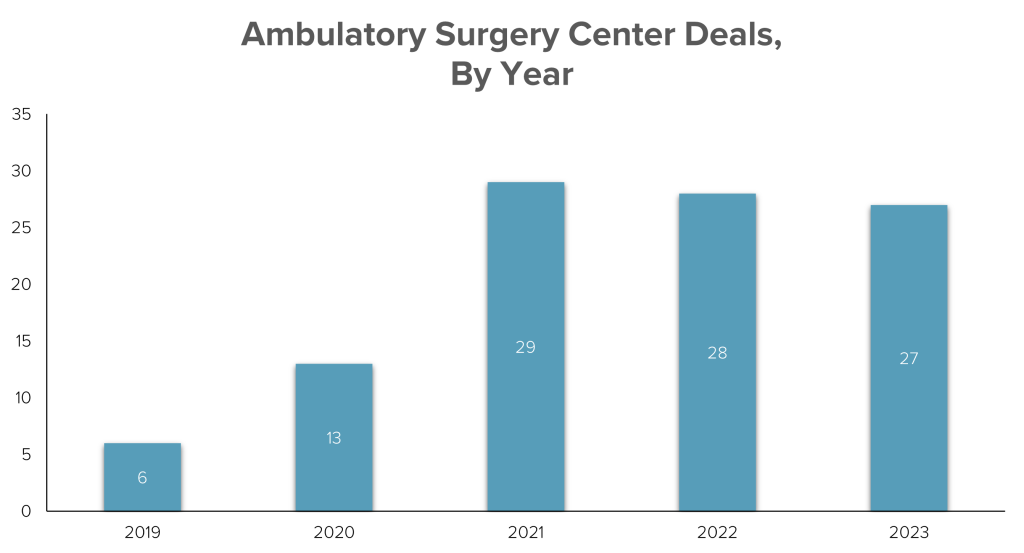

More than 80% of surgeries are now done in outpatient settings, according to the ASCA, and investors have caught onto this trend. There were 27 transactions targeting an ASC or ASC portfolio (31 properties in total) in 2023, and six in the first quarter of 2024, based on data captured in the LevinPro HC database. There is a vibrant mix of buyers in the field, from private equity (PE)-backed companies to real estate investment firms to health systems. This competition has kept the M&A market very active.

“Prices have leveled out, but we’re still seeing 5-7x or 7-9x multiples depending on the facility’s revenue and EBITDA range,” said J. Blake Peart, Managing Director at Vertess, a healthcare M&A advisory firm.

Peart has served as CEO for multiple hospitals, Fortune 500 companies, and several large ASCs, but now he serves as an advisor, often helping ASC owners find the right buyer in the market. We spoke with him about the ASC market and the different forces shaping the industry.

Two of the industry’s largest players, AmSurg (KKR) and Surgery Partners (Bain Capital), are both PE-backed. Bain Capital acquired a majority stake in Surgery Partners for $500 million in 2017, one of the largest transactions in the space ever, based on the disclosed purchase price at least.

“Strategic buyers will often acquire smaller ASCs with revenues of around $10 million,” said Peart. “There are also many PE-backed buyers in the market, and they often offer larger multiples.”

There are several notable tailwinds driving the ASC market, but investors need to be mindful of a few key areas as they look for opportunities.

As more Americans age, there is increasing demand for surgery center services. More than 49 million people, or 15% of the U.S. population, are now 65 or older. The share of Americans 65 and older will grow to 24% of the overall population by 2060. These demographic changes bode well for the ASC market, especially for specialties such as cardiology and orthopedics.

Geography also plays a major part in an ASC’s growth potential. If it’s an urban area with a large potential patient population, what is the competition? What are the neighboring health systems? And what does the referral network look like?

“If you’re a buyer in this market, you’ll need to examine the facility from a demographic and geographic standpoint,” said Peart. “Those areas will help you determine if the facility is poised for growth.”

States like Texas and California are usually hot markets for investors across several healthcare industries, but the competition in those regions can be fierce due to the number of ASC locations and the number of operators and health systems. There are nearly 900 ASCs across California alone, for instance.

The industry also remains highly fragmented. More than 70% of ASCs are still independently owned, with the remaining owned by large corporations. This gives a lot of room for both PE buyers and strategic investors to get a foothold in the market, especially as the industry moves toward outpatient offerings.

“2024 should be a strong year for any ASC that recovered well from COVID-19,” said Peart. “But size, scalability and physician presence should be top of mind for any buyer in the market.”

Schedule a demo today to see what LevinPro can do for your team.